Entities must assess the probability of a future event occurring that would confirm the existence of a liability. If it is probable that a liability has been incurred and the amount can be estimated, the entity is required to record a liability in its financial statements and disclose the nature of the contingency. If the contingent liability is consideredremote, it is unlikely to occur and may or may notbe estimable. This does not meet the likelihood requirement, andthe possibility of actualization is minimal. In this situation, nojournal entry or note disclosure in financial statements isnecessary.

How to Account for Potential Lawsuit Liability

Let’s continue to use Sierra Sports’ soccer goal warranty as our example. If the warranties are honored, the company should know how much each screw costs, labor cost required, time commitment, and any overhead costs incurred. This amount could be a reasonable estimate for the parts repair cost per soccer goal.

3: Define and Apply Accounting Treatment for Contingent Liabilities

Emotional distress—even though it includes physical symptoms such as insomnia, headaches, and stomach disorders—is not considered a physical injury or physical sickness. Therefore, settlement and award payments arising from claims for emotional distress are generally taxable. One important IFRS disclosure requirement that differs from US GAAP is the requirement to disclose movements in each class of provision (e.g. legal claims) during the reporting period. This rollforward schedule should distinguish amounts reversed and unused from amounts used. These amounts are computed claim by claim and cannot be netted against other provisions increases or decreases. In some cases, it may not be clear whether a present obligation exists, even if there is a past event – e.g. a legal claim that is disputed by the company.

MANAGING YOUR MONEY

- (e) When in the course of representation a lawyer is in possession of property in which two or more persons (one of whom may be the lawyer) claim interests, the property shall be kept separate by the lawyer until the dispute is resolved.

- The company is now very much smaller so it might simply not be necessary to run it on accrual anymore in which case I can just know that’s out there and not worry about the balance sheet.

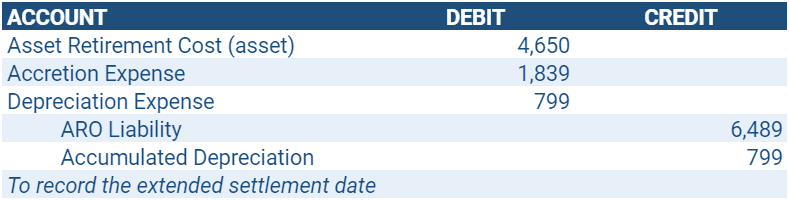

- Following are the necessary journal entries to record the expense in 2019 and the repairs in 2020.

- Past experience for the goals that thecompany has sold is that 5% of them will need to be repaired undertheir three-year warranty program, and the cost of the averagerepair is $200.

- However, under US GAAP, the accounting for related legal costs is subject to an accounting policy election.

When both of these criteria are met, the expected impact of the loss contingency is recorded. They believe that a loss is probable and that $800,000 is a reasonable estimation of the amount that will eventually have to be paid as a result of the damage done to the environment. Although this amount is only an estimate and the case has not been finalized, this contingency must be recognized. For example, assume that a business places an order with a truck company for the purchase of a large truck.

Not only does the contingentliability meet the probability requirement, it also meets themeasurement requirement. Warranties arise from products or services sold to customersthat cover certain defects (see Figure 12.8). It is unclear if a customer will need to use awarranty, and when, but this is a possibility for each product orservice sold that includes a warranty. The same idea applies toinsurance claims (car, life, and fire, for example), andbankruptcy. There is an uncertainty that a claim will transpire, orbankruptcy will occur. If the contingencies do occur, it may stillbe uncertain when they will come to fruition, or the financialimplications.

Recording a trust deposit as income

Acceptable accounting policies include expensing related costs as incurred or accruing related costs when they are deemed probable and reasonably estimable. Pending litigation involves legal claims against the business that may be resolved at a future point in time. The outcome of the lawsuit has yet to be determined but could have negative future impact on the business. journal entry for lawsuit settlement Any case with an ambiguous chance of success should be noted in the financial statements but doesn’t have to be listed on the balance sheet as a liability. Contingent assets are assets that are likely to materialize if certain events arise. These assets are only recorded in financial statements’ footnotes because their value can’t be reasonably estimated.

Be sure to record the transaction in your client’s account ledger, then deposit the payment in your firm’s operating account. Write any other checks to your client and third parties as required by the settlement statement. Every time you receive or disburse funds from a client’s trust account, you must notify your client. That means you must contact your client whenever you deposit money or withdraw money to cover incurred expenses or pay for fees that you’ve earned. You must give the client a statement of the services you rendered or the expenses you paid on their behalf. This statement must also show the amount you are withdrawing from the account to cover these costs.

When damages have been determined, or have been reasonably estimated, then journalizing would be appropriate. For our purposes, assume that Sierra Sports has a line of soccer goals that sell for $800, and the company anticipates selling 500 goals this year (2019). Past experience for the goals that the company has sold is that 5% of them will need to be repaired under their three-year warranty program, and the cost of the average repair is $200.

Leave a Reply